Topic 14 Logistic Regression & K-Nearest Neighbour (kNN) for Classification

This topic provides a brief introduction to two ML methods used for classification; Logistic Regression and K-Nearest Neighbour. The topic includes an example on predicting the direction of stock price movement to illustrate the application of R for these two models.

14.1 Logistic Regression

Logistic Regression belongs to the class of generalised linear models (glms)generalised linear models (glms)

Used to model data with a dichotomous response variable.

Logistic regression models the conditional probability of the response variable rather than its value.

A logit link function, defined as \(logit\,p=log[p/(1-p)]\), is used to transform the output of a linear regression to be suitable for probabilities.

A linear model for these transformed probabilities can be setup as

14.2 K-Nearest Neighbour

Nearest Neighbour classification (Quick Introduction)

Idea: Things that are alike are likely to have similar properties.

ML uses this principle to classify data by placing it in the same category or similar, or “nearest” neighbours.

Computers apply a human like ability to recall past experiences to make conclusions about current circumstances.

Nearest neighbour methods are based on a simple idea, yet they can be extremely powerful.

In general, well suited for classification tasks.

If a concept is difficult to define, but you know it when you see it, then nearest neighbours might be appropriate.

If the data is noisy and thus no clear distinction exists among the groups, nearest neighbour algorithms may struggle to identify the class boundaries.

k-NN Algorithm

K-nearest neighbor (KNN) is a very simple algorithm in which each observation is predicted based on its “similarity” to other observations.

The letter k is a variable term implying that any number of nearest neighbors could be used.

After choosing k, the algorithm requires a training dataset made up of examples that have been classified into several categories, as labeled by a nominal variable

Unlike most methods in ML, KNN is a memory-based algorithm and cannot be summarized by a closed-form model.

Measuring similarity in distance

Locating the nearest neighbours require a distance function; measuring similarity between two instances

k-NN uses Euclidean distance, a distance between two points. Euclidean distance is measured as the shortest direct route.

For p and q instances (to be compared) with n features

Choosing k

The balance between overfitting and underfitting the training data is a problem known as the bias-variance tradeoff.

Choosing a large k reduces the impact or variance caused by noisy data but can bias the learner such that it runs the risk of ignoring small, but important patterns.

There is no general rule about the best k as it depends greatly on the nature of the data.

A grid search can be performed to assess the best value of k

Grid Search: A grid search is an automated approach to searching across many combinations of hyperparameter values.

- A grid search would predefine a candidate set of values for k (e.g., k=1,2,…,j ) and perform a resampling method (e.g., k-fold CV) to estimate which k value generalizes the best to unseen data.

The caret package can be used to implement the knn method.

The next section demonstrate an application of Logistic Regression and KNN using an example from the applied finance domain.

14.3 Forecasting Stock Price Movement using ML

Topic-7 provided an introduction to using R for creating Technical Indicators for traded assets. This example uses selected indicators to predict the direction of the price movement, i.e., if the prices will be higher or lower the next day. Various studies have evaluated ML methods to predict the price direction or return, for example, Shynkevich, McGinnity, Coleman, Belatreche, & Li (2017) examined indicators like SMA, EMA etc on various forecast horizons and window lengths.

The example will use the closing prices of a stock (BHP in this case) to create the following Technical Indicators

Lag of 5 Days Simple Moving Average : Moving averages are the simplest among all indicators: they show the average price level for you on a rolling basis.

Lag 5 Days Exponential Moving Average: The difference between SMA and EMA is that SMA weighs all candles equally whereas EMA gives exponential weights – hence the name: it overweights recent days to previous ones.

MACD: Moving Average Convergence Divergence: Uses EMA of 26 and 12 days. Designed to reveal changes in strength, direction, momentum and duration of a trend in stock price.

Lag of Log Returns

Lag of RSI: Momentum oscillator that measures the speed and change of price movements. Ranges from zero to 100. Can be used to identify general trends.

The response (dependent) variable is constructed based on the previous day(s) prices. Here we use the following indicator:

14.3.1 Data & Indicators

library(quantmod)

library(TTR)

library(xts) #required as the data was saved as an xts object

d_bhp = readRDS("data/bhp_prices.rds")

d_bhp = d_bhp$BHP.AX.Close #select close prices

colnames(d_bhp) = "Price"

# SMA

sma5 = lag(SMA(d_bhp, n = 5)) #notice the use of the lag function to take lagged values

# EMA

ema5 = lag(EMA(d_bhp, n = 5))

# MACD

macd1 = lag(MACD(d_bhp))

# RSI

rsi1 = lag(RSI(d_bhp, 5))

# log returns

ret1 = lag(dailyReturn(d_bhp, type = "log"))

# price director indicator

dir = ifelse(d_bhp$Price >= lag(d_bhp$Price, 5), 1, 0) #direction variable compared to 5 day before price- Combine all the indicators and response variable in a data frame

d_ex1 = cbind(dir, ret1, sma5, ema5, macd1, rsi1)

# change column names

colnames(d_ex1) = c("Direction", "Ret", "SMA", "EMA", "MACD", "Signal",

"RSI")14.3.2 Visualise the data

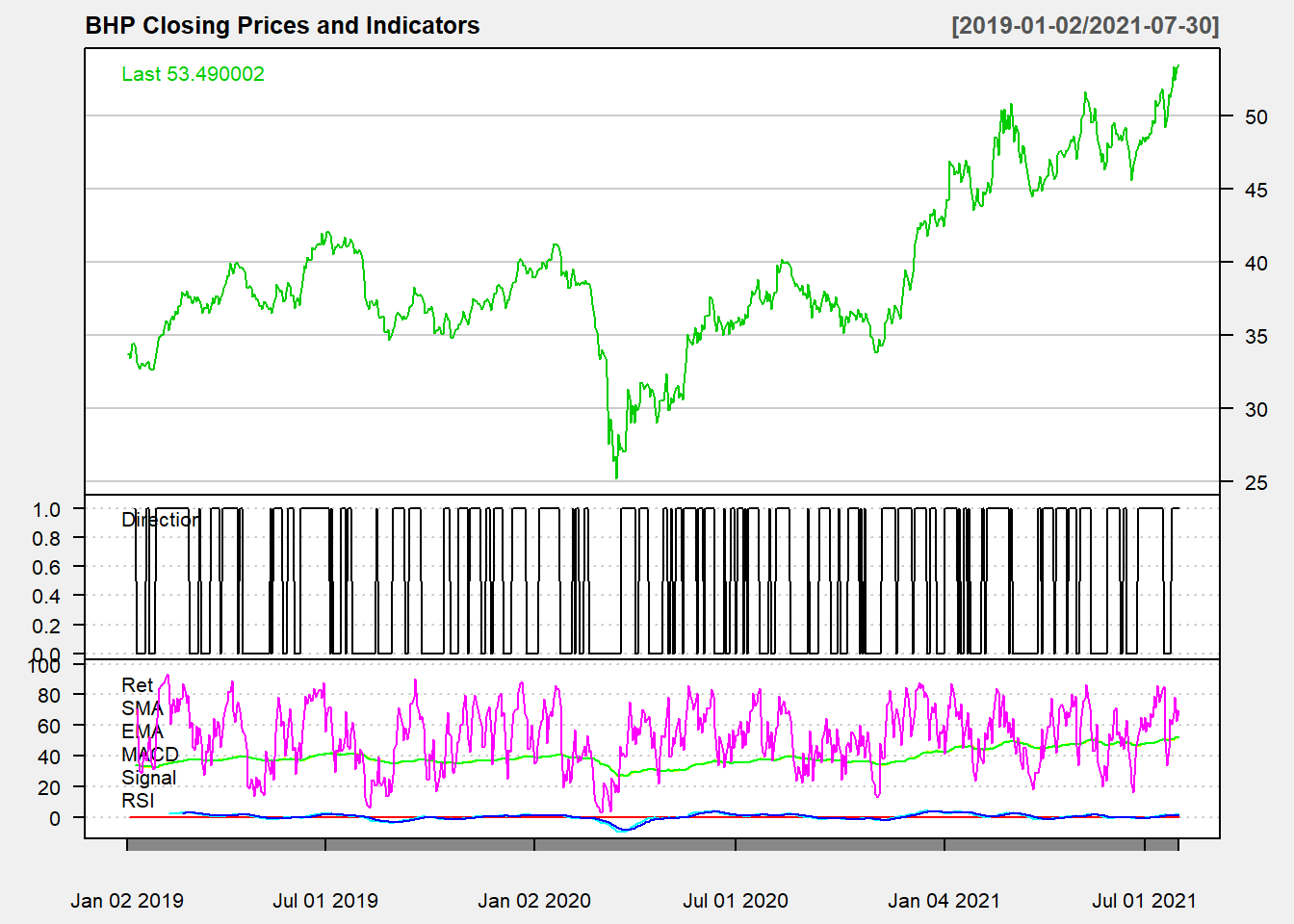

- Using the quantmod package

chartSeries(d_bhp, theme = "white", name = "BHP Closing Prices and Indicators")

addTA(d_ex1[, 1], col = 1, legend = "Direction") #Direction

addTA(d_ex1[, -1], on = NA, col = rainbow(6), legend = as.character(colnames(d_ex1[,

-1])))

Figure 14.1: Direction and Technical Indicators

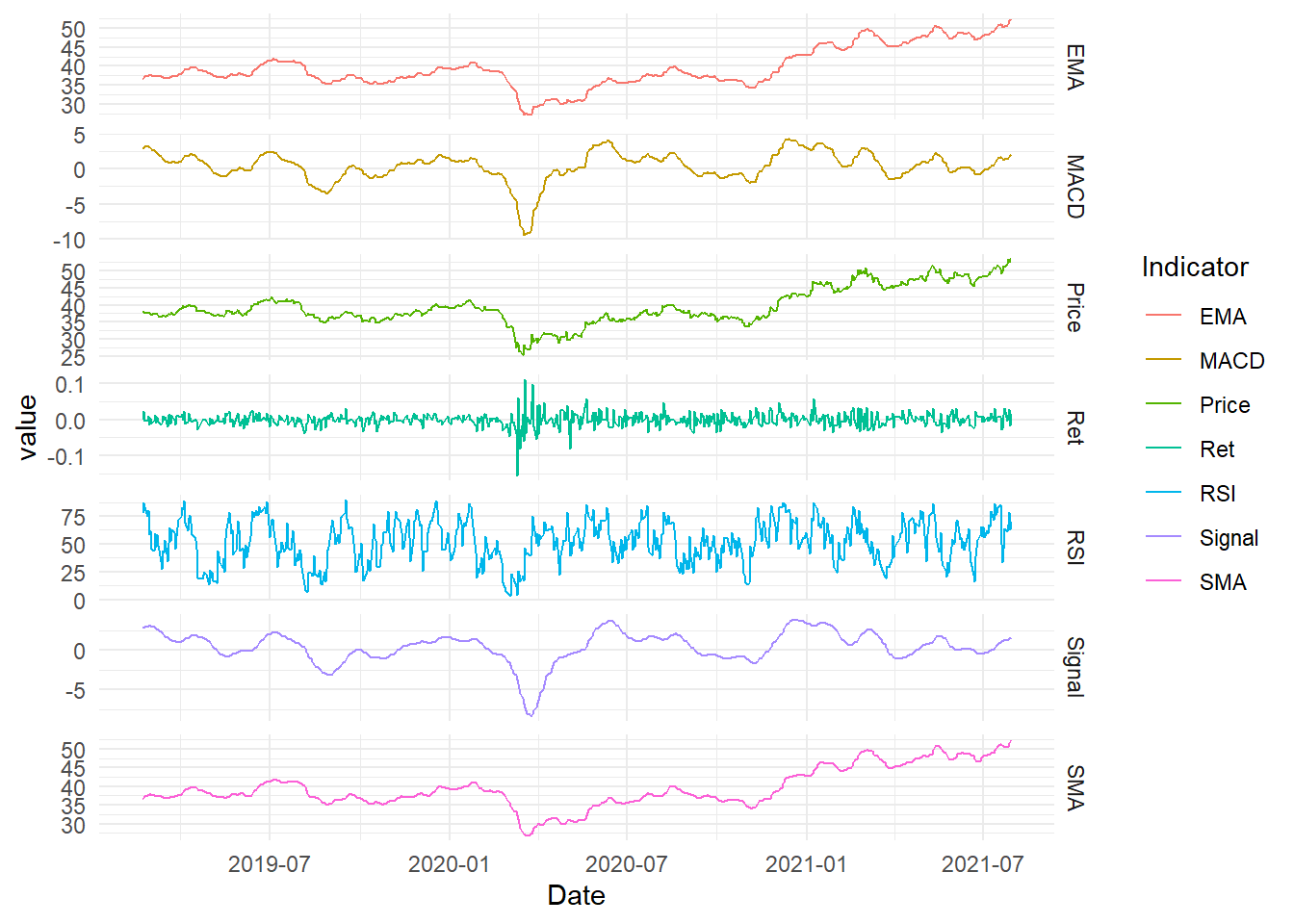

- The above graph can be improved using ggplot2

library(tidyr)

library(ggplot2)

# create a dataset and convert data to long

d_plot = merge.xts(d_bhp, d_ex1)

# remove NAs and then convert to long

d_plot = na.omit(d_plot)

# convert to dataframe

d_plot = data.frame(Date = index(d_plot), coredata(d_plot))

d_plot_long = pivot_longer(d_plot, -c(Date, Direction), values_to = "value",

names_to = "Indicator")

# change direction to a factor

d_plot_long$Direction = as.factor(d_plot_long$Direction)

(p2_ex = ggplot(d_plot_long, aes(Date, value, color = Indicator)) + geom_path(stat = "identity") +

facet_grid(Indicator ~ ., scale = "free") + theme_minimal())

Figure 14.2: Indicators and Prices (ggplot2)

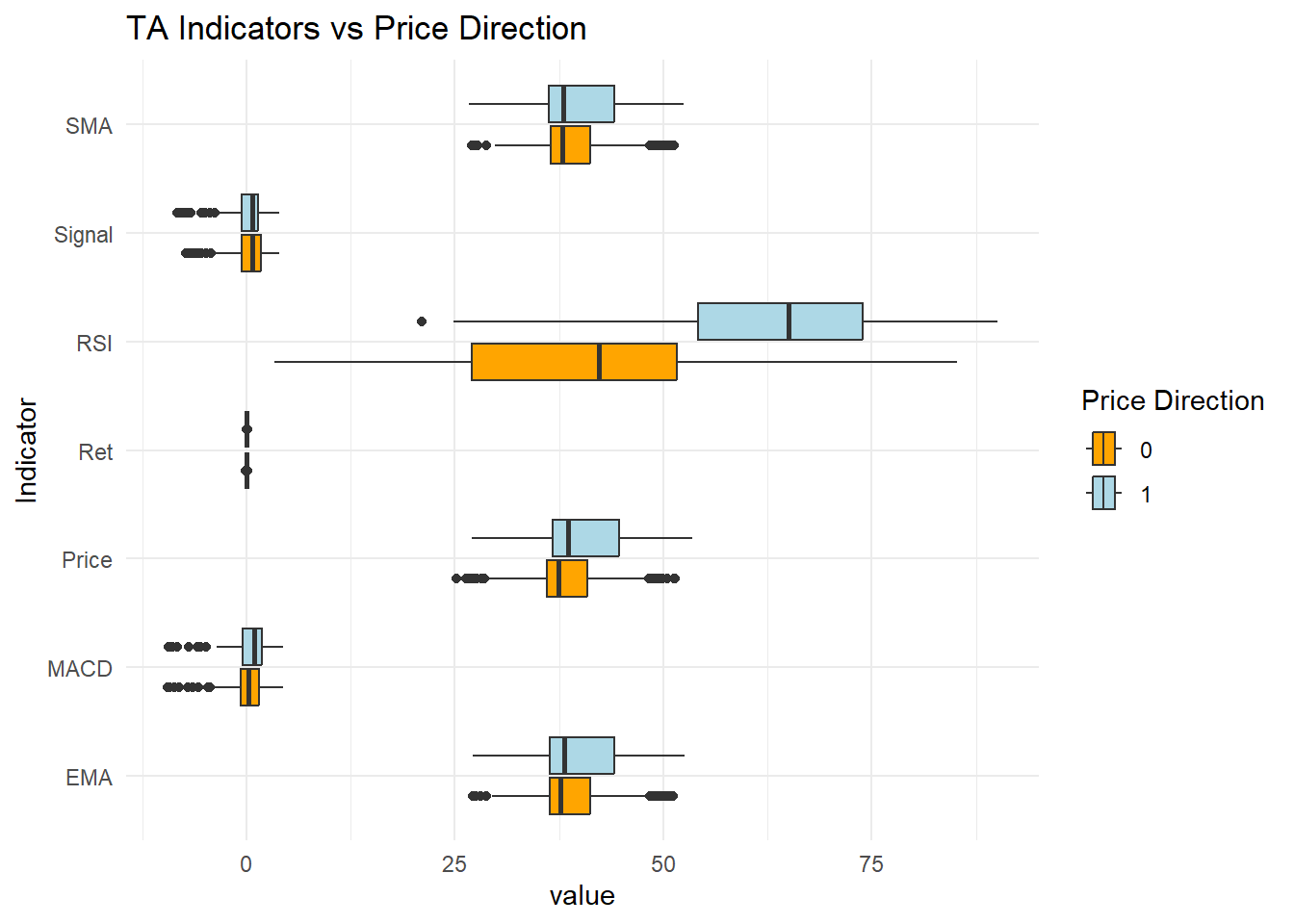

- The above is a line chart of indicators and prices. We can also create a box plot to visualise the variance in the values relative to the direction

p2_ex = ggplot(d_plot_long, aes(value, Indicator, fill = Direction)) +

geom_boxplot()

p2_ex + theme_minimal() + labs(title = "TA Indicators vs Price Direction") +

scale_fill_manual(name = "Price Direction", values = c("orange", "lightblue"))

Figure 14.3: Box Plot of Indicators

- Some differences per category can be noticed

14.3.3 Using Logistic Regression

- 70:30 data split

- Time series sampling

- Stratified sampling will not keep the time order and hence its avoided

# remove NAs

d_ex1 = na.omit(d_ex1)

# convert to data frame

d_ex1 = as.data.frame(d_ex1)

# convert direction to a factor for classification

d_ex1$Direction = as.factor(d_ex1$Direction)

idx1 = c(1:round(nrow(d_ex1) * 0.7)) #create index for first 70% values to be in the testing set

d_train1 = d_ex1[idx1, ] #training set

d_test1 = d_ex1[-idx1, ] #testing setTraining Setup

- Time series cross validate for resampling: 250 day window 30 days for prediction (this can be changed)

- Data preprocessing is conducted to normalise the scale of the values

glmmethod with binomial family for the binary classification

library(caret)

set.seed(999)

# control

cntrl1 = trainControl(method = "timeslice", initialWindow = 250, horizon = 30,

fixedWindow = TRUE)

# preprocesing

prep1 = c("center", "scale")

# logistic regression

logit_ex1 = train(Direction ~ ., data = d_train1, method = "glm", family = "binomial",

trControl = cntrl1, preProcess = prep1)

logit_ex1 #final model accuracyGeneralized Linear Model

434 samples

6 predictor

2 classes: '0', '1'

Pre-processing: centered (6), scaled (6)

Resampling: Rolling Forecasting Origin Resampling (30 held-out with a fixed window)

Summary of sample sizes: 250, 250, 250, 250, 250, 250, ...

Resampling results:

Accuracy Kappa

0.7324731 0.4658076summary(logit_ex1$finalModel) #summary of the final model

Call:

NULL

Deviance Residuals:

Min 1Q Median 3Q Max

-2.43299 -0.63007 -0.04745 0.57603 2.49565

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -0.05772 0.13429 -0.430 0.667

Ret -0.82494 0.18720 -4.407 1.05e-05 ***

SMA -20.20397 3.70217 -5.457 4.83e-08 ***

EMA 20.05707 3.67374 5.460 4.77e-08 ***

MACD 0.50610 0.73203 0.691 0.489

Signal -0.94914 0.68541 -1.385 0.166

RSI 2.14092 0.30037 7.128 1.02e-12 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 601.61 on 433 degrees of freedom

Residual deviance: 348.17 on 427 degrees of freedom

AIC: 362.17

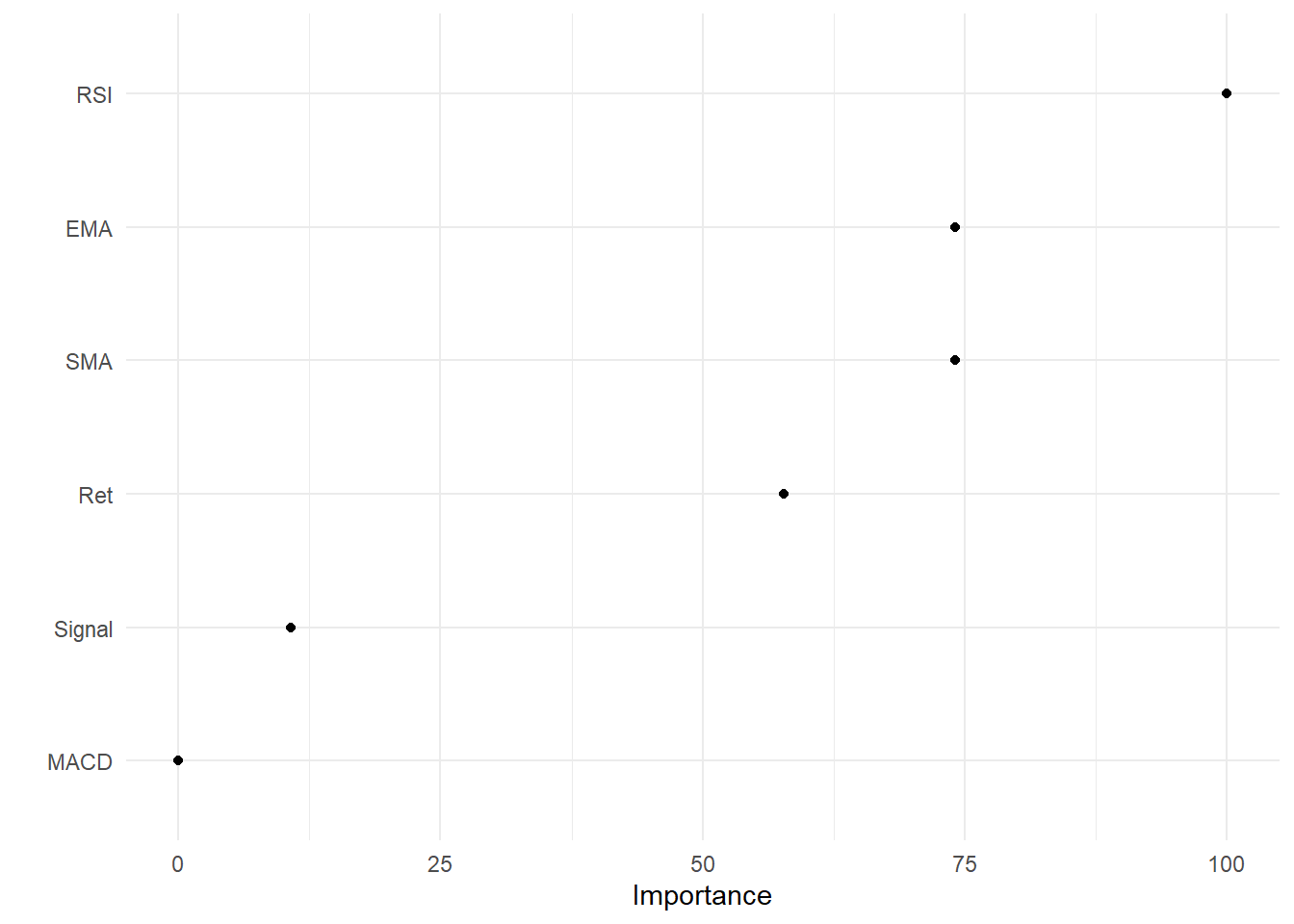

Number of Fisher Scoring iterations: 5- Variable importance

- In the case of multiple predictor variables, we want to understand which variable is the most influential in predicting the response variable.

library(vip)

vip(logit_ex1, geom = "point") + theme_minimal()

Figure 14.4: Variable Importance

Predictive Accuracy

- ML models should be checked for predictive accuracy on the test set

- caret provides

predictfunction to create predictions - These predictions can be assessed based on the confusion matrix

Confusion Matrix - When applying classification models, we often use a confusion matrix to evaluate certain performance measures.

A confusion matrix is simply a matrix that compares actual categorical levels (or events) to the predicted categorical levels.

Prediction of the right level; refer to this as a true positive.

Prediction of a level or event that did not happen this is called a false positive (i.e. we predicted a customer would redeem a coupon and they did not).

Alternatively, when we do not predict a level or event and it does happen that this is called a false negative (i.e. a customer that we did not predict to redeem a coupon does).

Let’s predict using the final model and assess using the confusion matrix.

pred1 = predict(logit_ex1, newdata = d_test1) #prediction on the test data

confusionMatrix(data = pred1, reference = d_test1$Direction)Confusion Matrix and Statistics

Reference

Prediction 0 1

0 52 26

1 16 92

Accuracy : 0.7742

95% CI : (0.7073, 0.8321)

No Information Rate : 0.6344

P-Value [Acc > NIR] : 2.959e-05

Kappa : 0.5279

Mcnemar's Test P-Value : 0.1649

Sensitivity : 0.7647

Specificity : 0.7797

Pos Pred Value : 0.6667

Neg Pred Value : 0.8519

Prevalence : 0.3656

Detection Rate : 0.2796

Detection Prevalence : 0.4194

Balanced Accuracy : 0.7722

'Positive' Class : 0

- The model provides decent accuracy which is higher than the No Information Rate and also statistically significant.

There are other analyses which can be conducted on logistic regression, for example, ROC (Receiver Operating Characteristic) curve analysis for the Area Under the Curve.

14.3.4 Using K-NN

- This section will implement the previous model using k-nearest neigbour algorithm using the caret package

- Then we will use the same split as the logistic regression

- We are selecting the model based on Accuracy & Kappa

- Accuracy: Accuracy measures the overall correctness of the classifier \(\frac{(TN+TP)}{Total}\). Objective: maximise

- Kappa (Cohen’s Kappa): Its like Accuracy but it is normalised at the baseline of random chance on the dataset. It compares observed accuracy to expected accuracy.

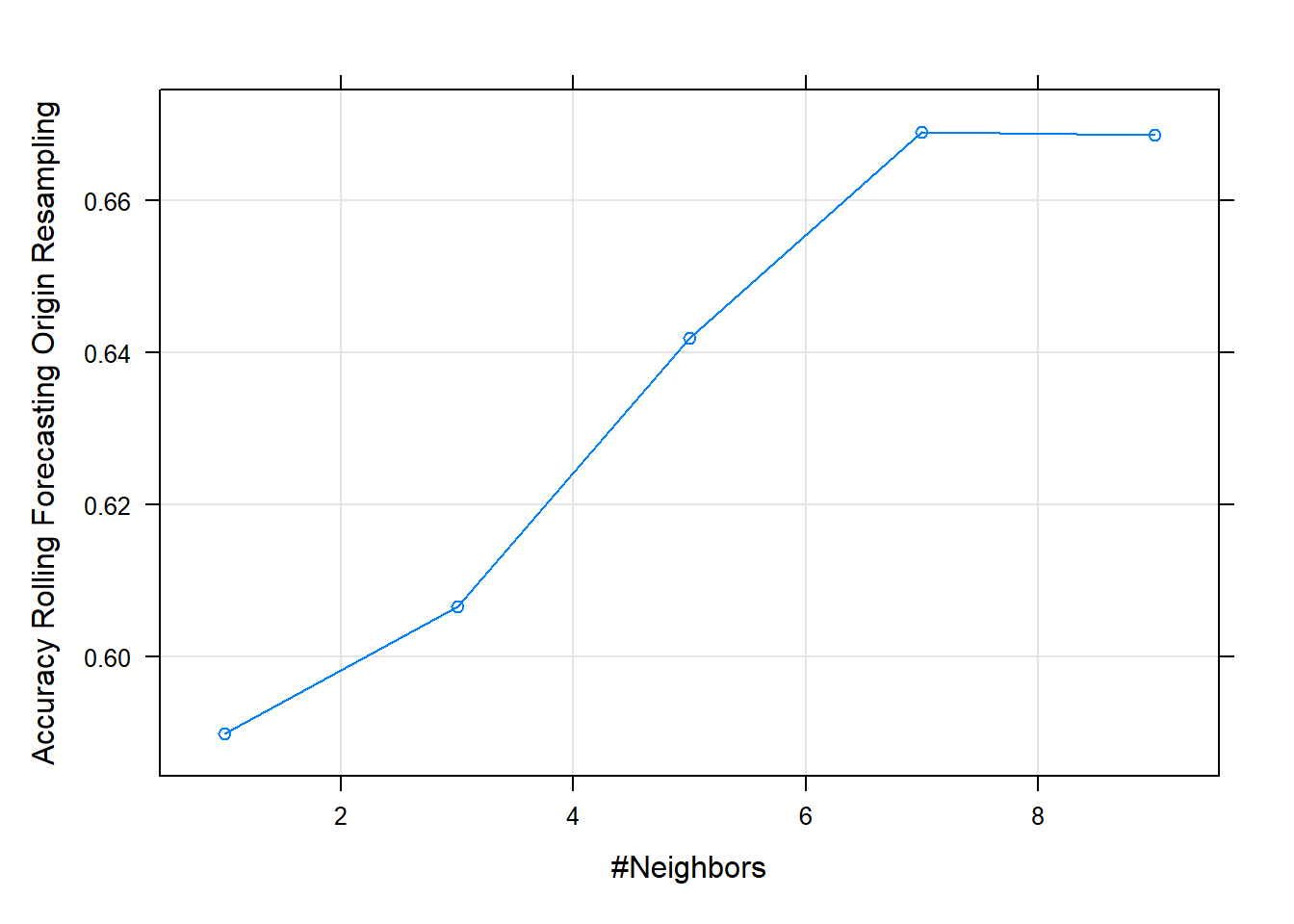

- A grid search is used to search for an optimal value for k

set.seed(999)

grid1 = expand.grid(k = seq(1, 10, by = 2)) #to search from k=1 to k=10

knn_ex1 = train(Direction ~ ., data = d_train1, method = "knn", tuneGrid = grid1,

trControl = cntrl1, preProcess = prep1)- View the fit

plot(knn_ex1) #may suggest using a wider grid

Figure 14.5: Grid plot

knn_ex1k-Nearest Neighbors

434 samples

6 predictor

2 classes: '0', '1'

Pre-processing: centered (6), scaled (6)

Resampling: Rolling Forecasting Origin Resampling (30 held-out with a fixed window)

Summary of sample sizes: 250, 250, 250, 250, 250, 250, ...

Resampling results across tuning parameters:

k Accuracy Kappa

1 0.5898925 0.1554741

3 0.6066667 0.1834679

5 0.6419355 0.2500894

7 0.6690323 0.3194890

9 0.6686022 0.3209926

Accuracy was used to select the optimal model using the largest value.

The final value used for the model was k = 7.Variable importance can’t be obtained here as KNN does not produce a model

Predictive Accuracy

Let’s predict using the final model and assess using the confusion matrix.

pred2 = predict(knn_ex1, newdata = d_test1) #prediction on the test data

confusionMatrix(data = pred2, reference = d_test1$Direction)Confusion Matrix and Statistics

Reference

Prediction 0 1

0 50 50

1 18 68

Accuracy : 0.6344

95% CI : (0.5608, 0.7037)

No Information Rate : 0.6344

P-Value [Acc > NIR] : 0.5330295

Kappa : 0.2833

Mcnemar's Test P-Value : 0.0001704

Sensitivity : 0.7353

Specificity : 0.5763

Pos Pred Value : 0.5000

Neg Pred Value : 0.7907

Prevalence : 0.3656

Detection Rate : 0.2688

Detection Prevalence : 0.5376

Balanced Accuracy : 0.6558

'Positive' Class : 0

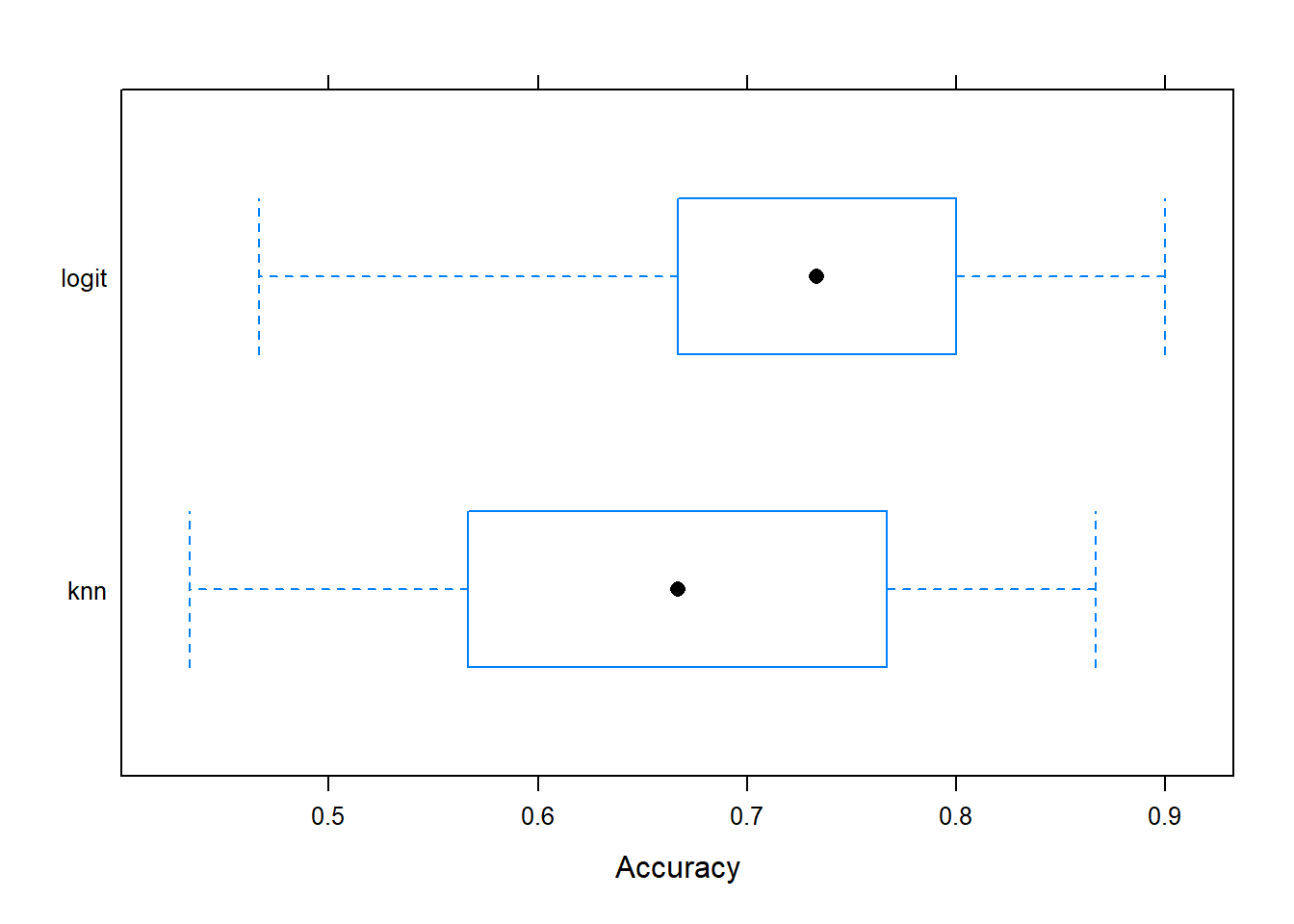

A comparison betweek Logistic Regression and KNN can be made based on their predictive accuracy.

The two models can also be compared based on their resampling results.

The random number seeds should be initialised to the same value for resampling comparison.

The following code compares the model fits.

resamp1 = resamples(list(logit = logit_ex1, knn = knn_ex1))

summary(resamp1)

Call:

summary.resamples(object = resamp1)

Models: logit, knn

Number of resamples: 155

Accuracy

Min. 1st Qu. Median Mean 3rd Qu. Max. NA's

logit 0.4666667 0.6666667 0.7333333 0.7324731 0.8000000 0.9000000 0

knn 0.4333333 0.5666667 0.6666667 0.6690323 0.7666667 0.8666667 0

Kappa

Min. 1st Qu. Median Mean 3rd Qu. Max. NA's

logit 0.1208791 0.3333333 0.4666667 0.4658076 0.5838144 0.7887324 0

knn -0.1860465 0.1558442 0.3243243 0.3194890 0.4666667 0.7235023 0bwplot(resamp1, metric = "Accuracy")

Figure 14.6: Resample Accuracy comparison

- The graph provides a comparison of the overall accuracy of the model (not the predictions).